.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

Study Takeaways

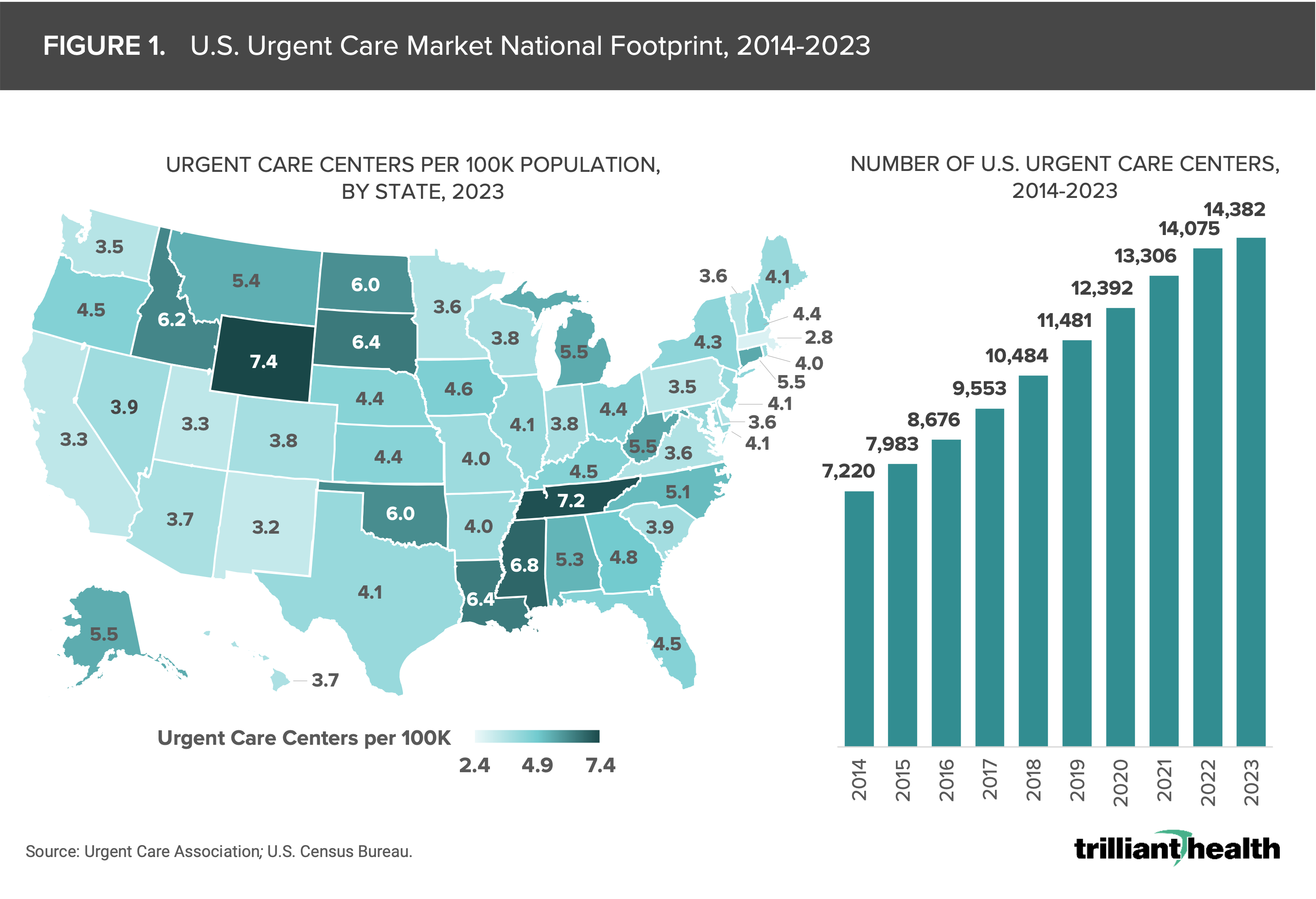

- From 2014 to 2023, the number of urgent care centers in the U.S. increased by almost 100%, from 7,220 in 2014 to 14,382 as of the middle of 2023.

- Excluding COVID-19 visit volumes, urgent care utilization increased by 18.9% from Q2 2019 to Q2 2023 as compared to the 25.2% increase in the number of U.S. urgent care centers during the same period, suggesting that supply of urgent care clinics is outpacing demand.

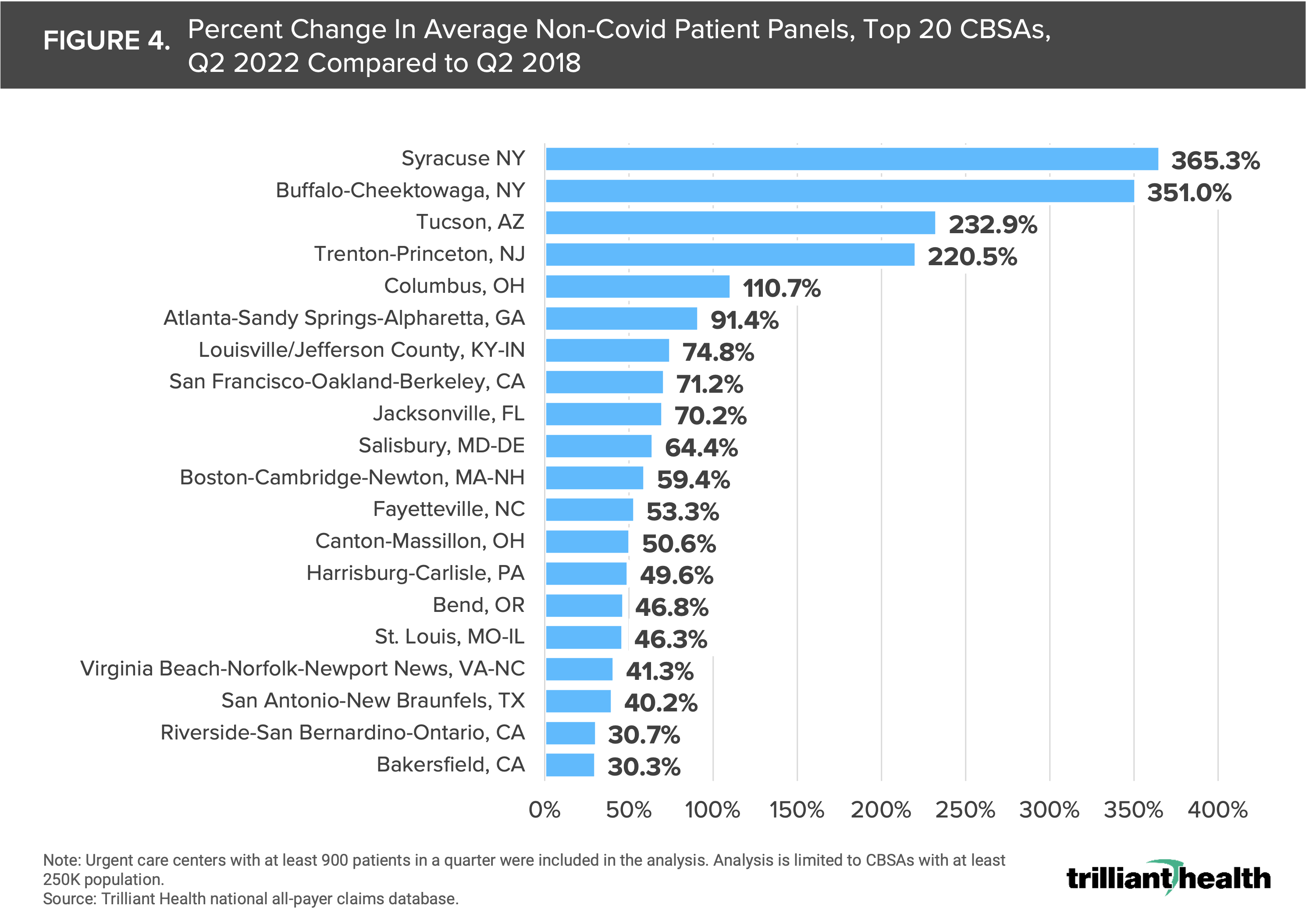

- From Q2 2018 to Q2 2023, urgent care centers in the Syracuse, NY and Buffalo, NY metropolitan areas saw the highest growth in average non-COVID-19 patient panels, while Fort Wayne, IN and Tallahassee, FL metropolitan areas saw the greatest decline.

- Non-COVID visit reasons have remained consistent over time, with acute respiratory illnesses accounting for the top six visit reasons, followed by urinary issues, joint pain and abdominal pain.

Recently, we analyzed the distribution of low-acuity care across three large geographic markets, focusing on urgent care, traditional primary care providers and new entrants such as Walmart.1 Our findings concluded that new entrants deliver less than 1% of low-acuity care, while urgent care's share has steadily increased over time in these select markets. Countless pivots within Amazon's healthcare division over the past few years, Walgreens’ rapid closure of VillageMD sites and the abrupt shuttering of all Walmart Health locations highlight the challenges of delivering low-acuity care while maintaining financial viability.2,3,4

Once considered a “disruptor” in redirecting low-acuity and non-emergent care, urgent care facilities have evolved and matured to the point where many consider urgent care to be a “traditional” provider setting. Because of the dramatic change in urgent care utilization during the pandemic, we wanted to explore the sustained changes and evolution in post-pandemic consumer utilization of urgent care facilities.

Background

While the first urgent care centers emerged in the 1970s, it took decades for the market to mature and integrate with the broader U.S. healthcare system. For many years, consumers were hesitant to visit urgent care centers because of perceptions about quality.

In the last two decades, the sector has experienced significant growth, driven by the widening primary care gap and increasing consumer demand for on-demand and convenient healthcare.5 From 2014 to 2023, the number of urgent care centers in the U.S. nearly doubled, increasing by 99.2% from 7,220 to 14,382 (Figure 1). This growth trajectory is expected to continue.6

While there is demand for urgent care supply across all U.S. markets, the distribution of urgent care centers varies by state. Analyzing the per capita concentration of urgent care centers, urgent care is most highly concentrated in Wyoming (7.4 centers per 100K population) and least concentrated in the District of Columbia (2.4 centers per 100K population).

During the pandemic, consumers largely ignored initial guidance from regulators encouraging patients not to seek COVID-19 testing at urgent care centers or emergency departments, which resulted in dramatic volume increases across the country.7 Notably, visit types that were characteristic of urgent care centers pre-pandemic such as urinary tract infections and ear infections declined over the same period.

The tapering of COVID-19 testing and treatment volumes and continued growth in the number of urgent care centers prompted us to examine changes in urgent care demand and patient panels over time.

Analytic Approach

Leveraging our national all-payer claims database, we analyzed urgent care utilization between Q1 2018 and Q2 2023 and segmented by visits for COVID-19 (i.e., testing or treatment) and all other reasons. We also analyzed the average quarterly patient panel – defined as the average number of patients seen at an urgent care in a quarter – at all U.S. urgent care centers with at least 900 patients in a given quarter, both nationally and for select markets.

Findings

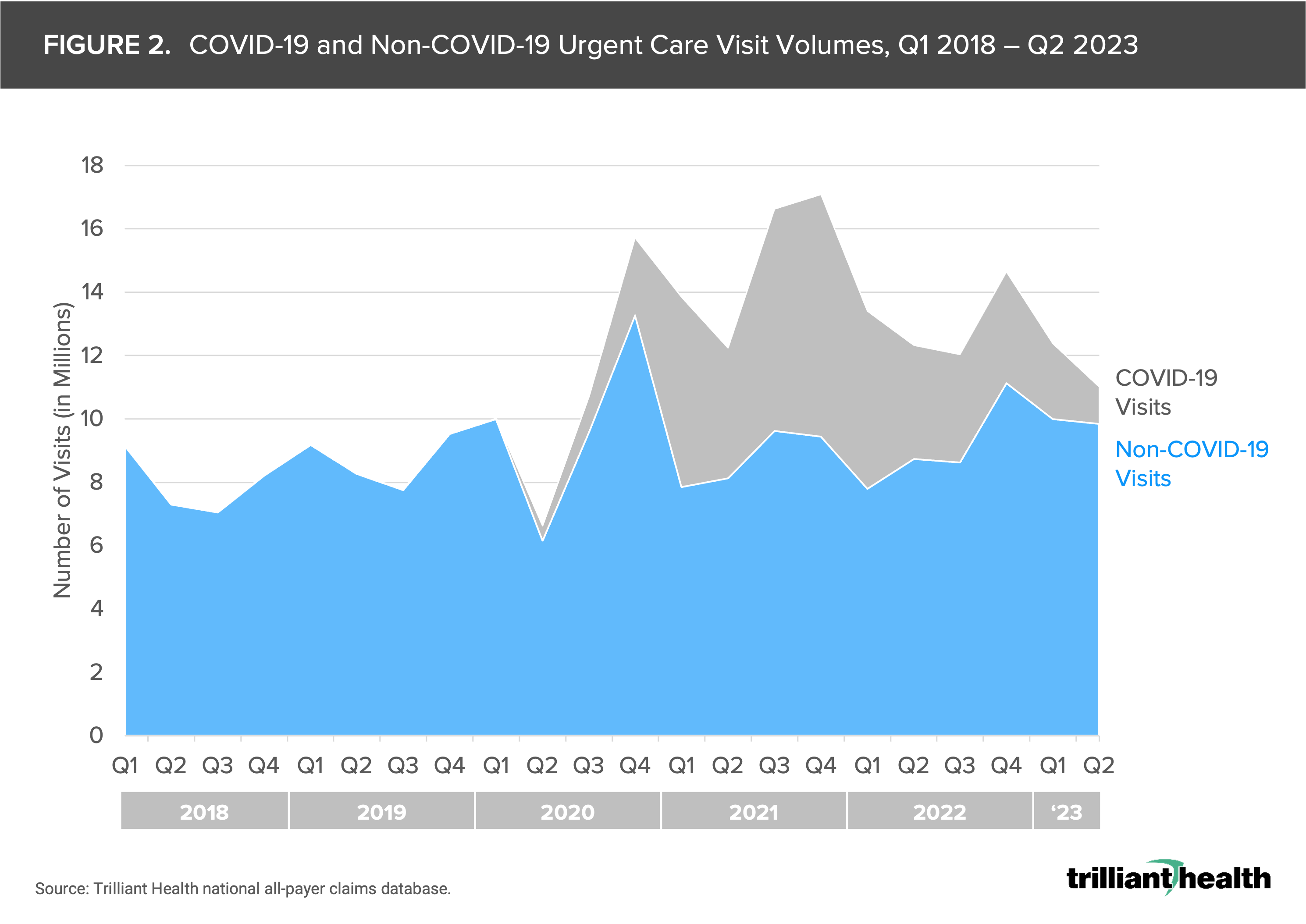

In Q2 2020, non-COVID-19 urgent care visit volumes dropped by 38.4% from the preceding quarter and were 15.5% lower than in Q2 2018 (Figure 2), which is unsurprising based on Federal, state and local guidance to avoid any non-emergent treatment.

In contrast, at the peak of urgent care utilization in Q4 2021, all urgent care visit volumes were 108.0% higher than in Q4 2018, but 44.7% of those Q4 2021 visits were attributed to COVID-19 reasons.

Excluding COVID-19 visit volumes, urgent care utilization increased by 18.9% from Q2 2019 to Q2 2023 as compared to the 25.2% increase in the number of U.S. urgent care centers during the same period, suggesting that supply of urgent care clinics is outpacing demand.

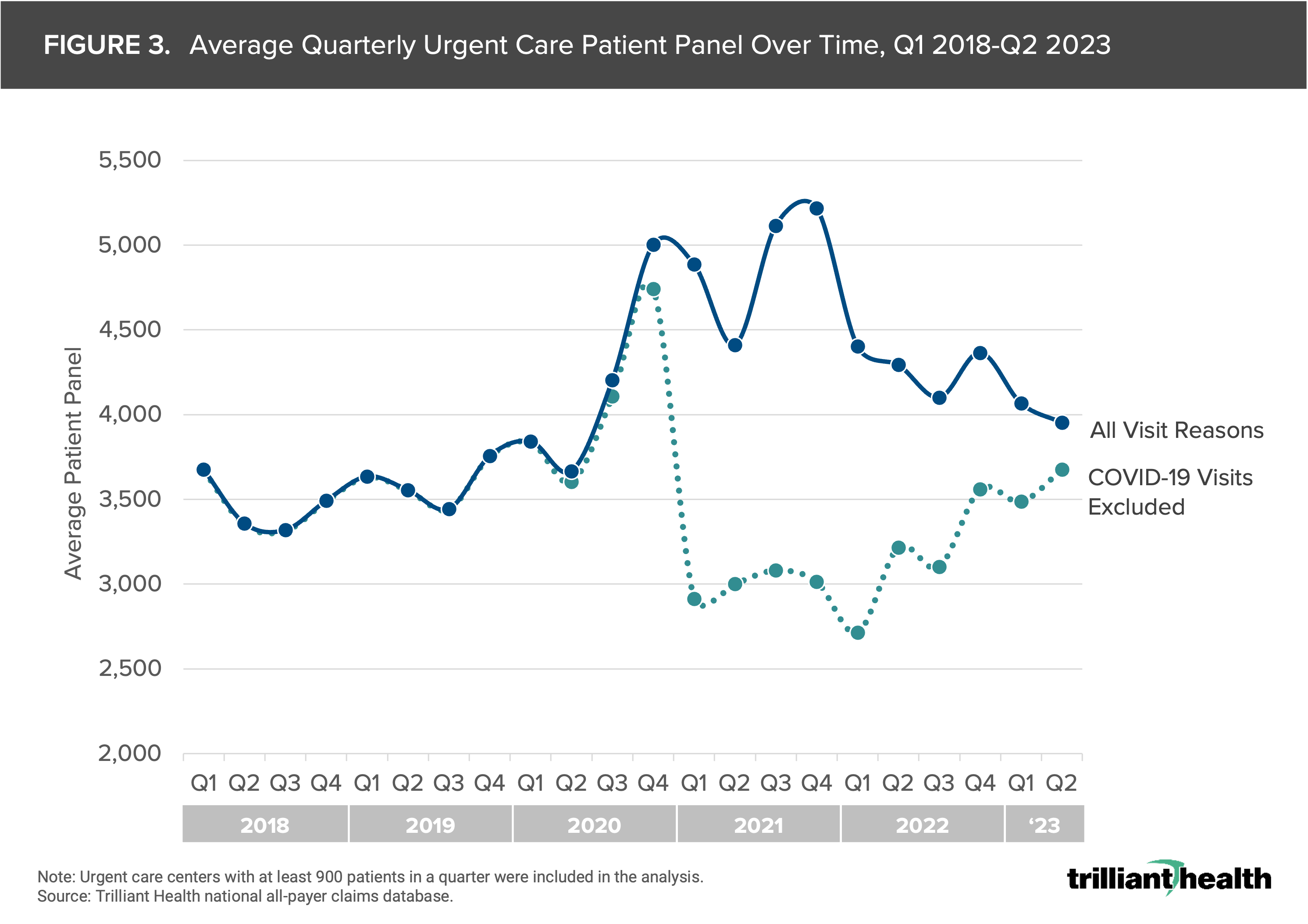

Average quarterly patient panels at U.S. urgent care centers for all visit reasons spiked in Q4 2020, increasing by 30.2% from Q1 2020, the quarter immediately preceding the declaration of the Public Health Emergency (Figure 3).

However, following a peak in Q4 2021, average patient panels declined over the following quarters. Notably, with COVID-19 patients excluded, average patient panels trended well below pre-pandemic averages. By Q2 2023, non-COVID-19 average patient panels appeared to have rebounded, 3.5% higher compared to Q2 2019.

Market-Level Changes in Urgent Care Patient Panels and Top Visit Reasons

We analyzed markets that saw the highest and lowest percentage change in non-COVID-19 patient panels from Q2 2018 to Q2 2023. Urgent care centers in the Syracuse, NY and Buffalo, NY metropolitan areas saw the highest growth in average patient panels, increasing by 365.3% and 351.0%, respectively (Figure 4).

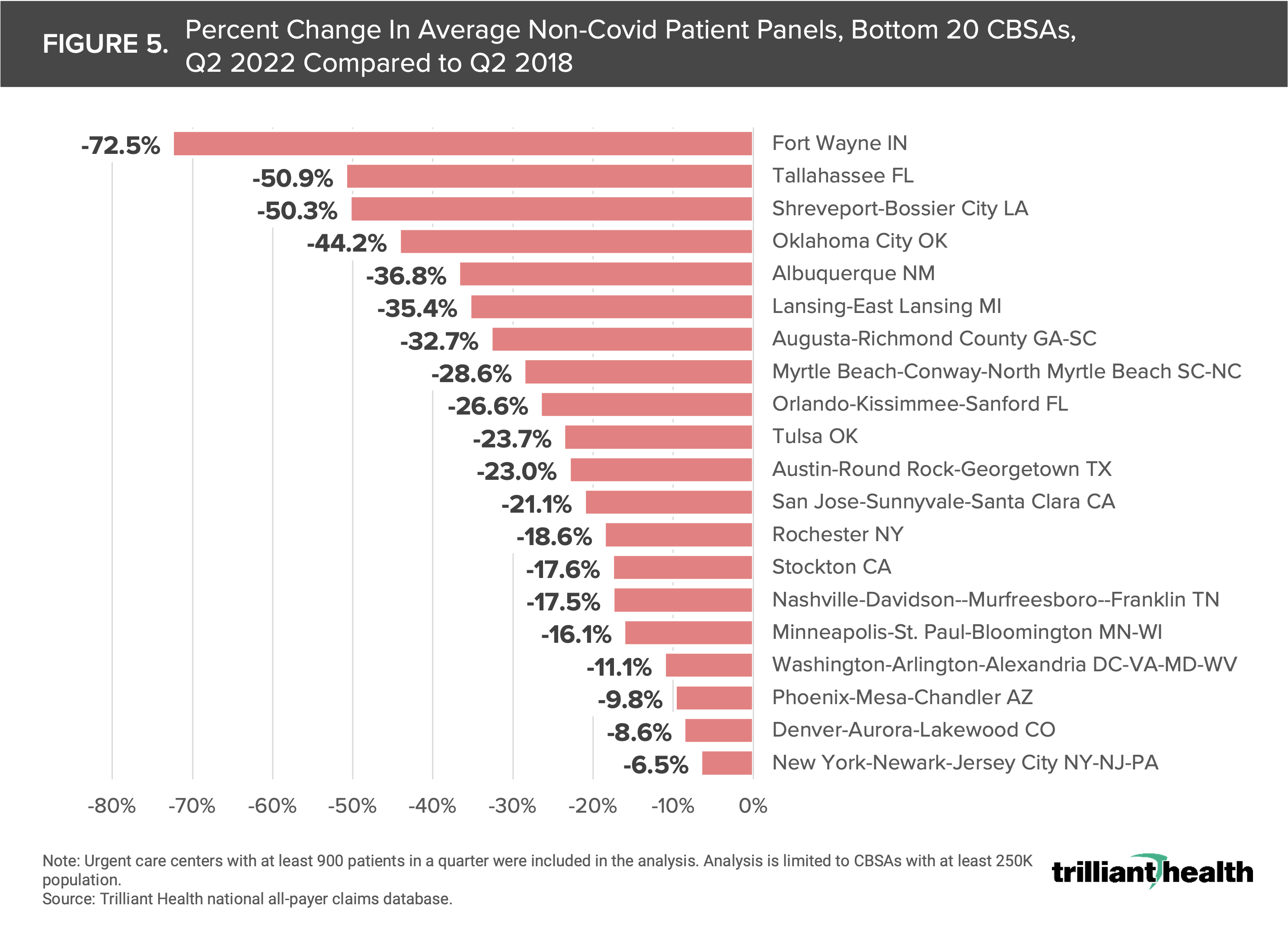

On the other hand, urgent care centers in the Fort Wayne, IN and Tallahassee, FL metropolitan areas saw the greatest decline in average patient panels, decreasing by 72.5% and 50.9%, respectively (Figure 5).

To what extent is the substantial growth in these markets – and decline in others – attributed to changes in demand? Or consumer preferences? Or urgent care and staffed provider supply?

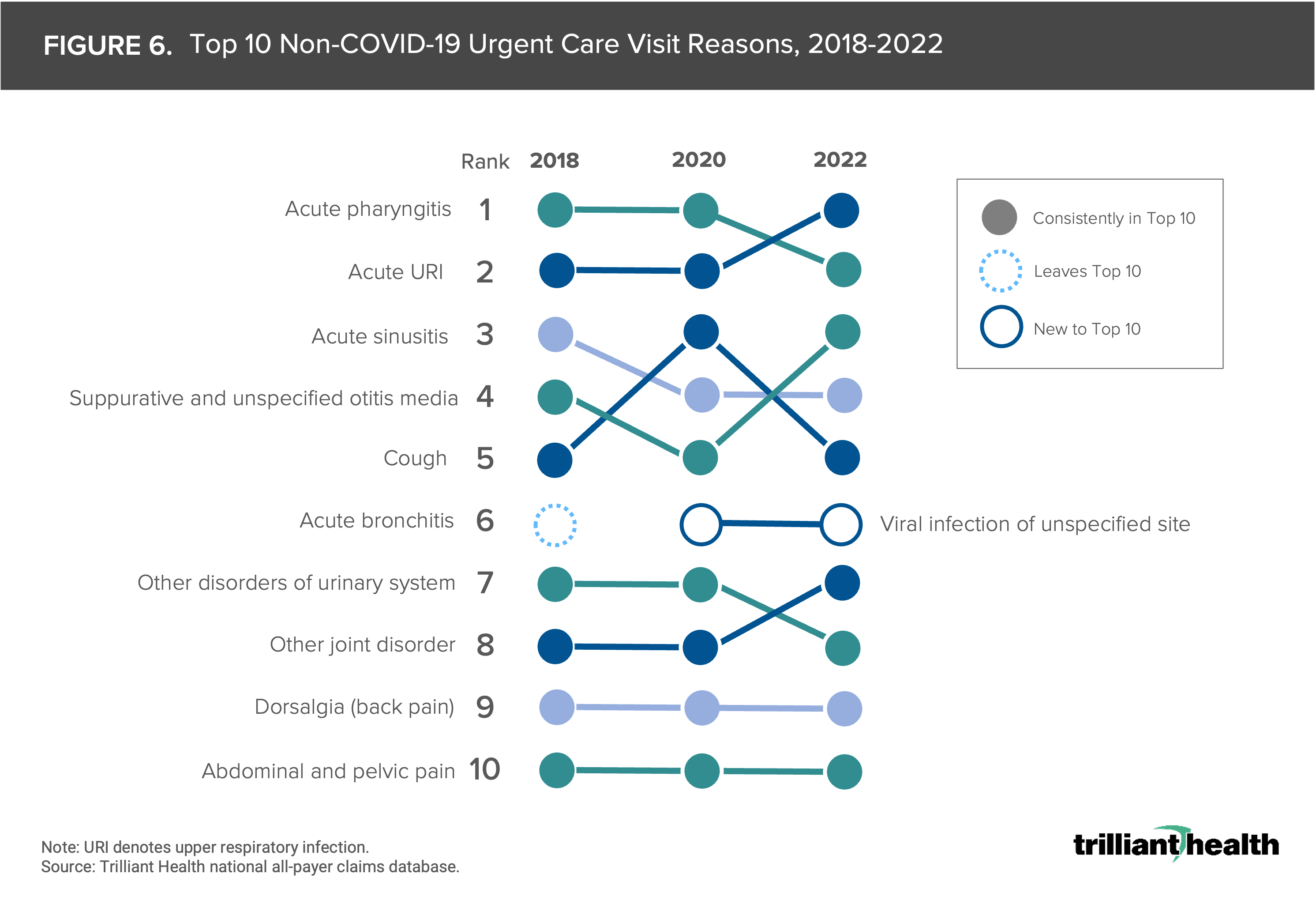

While COVID-19 testing and treatment topped the reasons for seeking urgent care in 2020 and 2021, the top non-COVID-19 reasons for seeking urgent care have remained largely consistent over time. The services rendered at urgent care centers are generally consistent across sites of care, resulting in a consistent list of most common visit reasons. Acute respiratory illnesses have always accounted for the top six visit reasons, followed by urinary conditions, joint or back pain and abdominal or back pain (Figure 6).

Conclusion

The COVID-19 pandemic inflated urgent care patient volumes, overwhelming urgent care centers nationwide, while simultaneously reshaping the landscape of patient demand and care provision.

Our findings reveal a mismatch between urgent care demand and supply relative to the growth in urgent care centers over the last few years. While the number of urgent care centers has steadily increased, non-COVID-19 visit volumes fluctuated, with periods of decline followed by peaks in utilization. Furthermore, average patient panels also saw fluctuations, peaking during the pandemic before declining in subsequent quarters.

While the average non-COVID-19 patient panel has seemed to normalize compared to pre-pandemic, to what extent does this vary regionally, and how will that trend evolve in the coming years as the healthcare system undergoes continued transformation? The artificially increased demand for urgent care during the COVID-19 pandemic may have inclined consumers to consider urgent care for other aspects of their healthcare needs in a way they might not have otherwise.

In response to the COVID-19 pandemic, many urgent care providers introduced virtual care services. The most common reasons for visits (e.g., common respiratory illnesses) have largely remained unchanged over time, and many can be addressed via telehealth. However, with several large-scale telehealth operators exiting the market, it remains to be seen whether urgent care providers will continue to expand their virtual capabilities or instead return to a focus on in-person care. Additionally, the struggles that large retailers have faced in scaling low-acuity care delivery in urban and suburban areas begs the question of whether the urgent care market had been sufficiently meeting that market demand.

In our 2022 analysis of the urgent care market, we concluded that stakeholders underestimate the extent to which basic medical care was lost during the pandemic and, in turn, the potentially more acute disease progression for patients whose care needs were initially non-emergent and non-life threatening.8 While urgent care centers clearly cater to demand for low-acuity illnesses, preventive primary demand continues to track below pre-pandemic levels, underscoring the need for multi-stakeholder intervention to address these gaps, particularly in low-income and rural areas. Stakeholders need to think critically about how to re-engage patients and halt the growing disintermediation and fragmentation of healthcare, which ultimately sacrifices consumer health status for convenience.

Get the latest insights delivered to your inbox.

Related Research

Was this shared with you?

Subscribe for weekly insights.

Subscribe to receive weekly insights from Trilliant Health's Research Team

Interested in citing our research? Please follow this guide.