.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

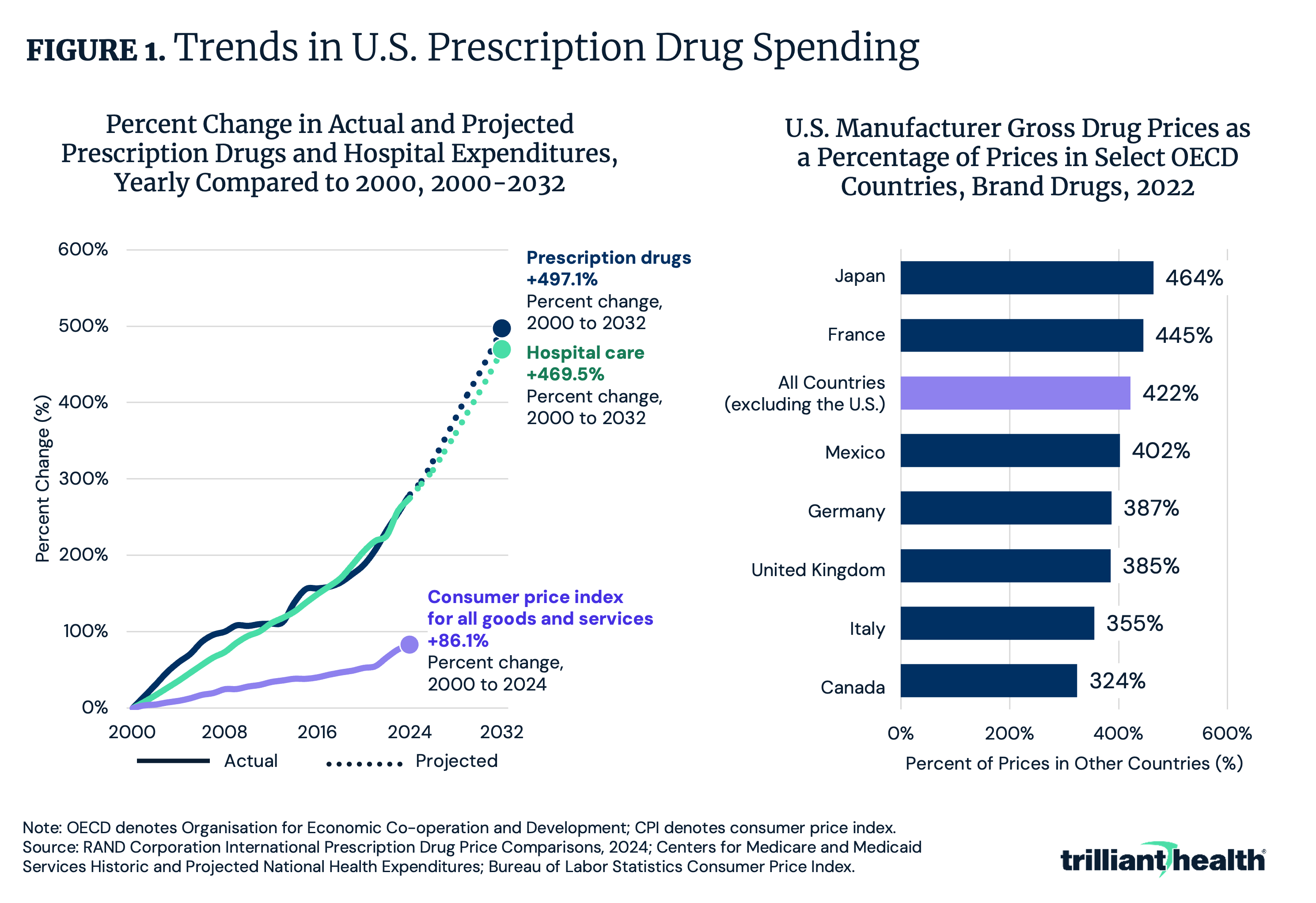

- In 2022, the U.S. paid on average 422% more for branded prescription drugs than other OECD countries. Prescription drug expenditures have increased more than 200% since 2000 and are projected to double again from 2024 to 2032.

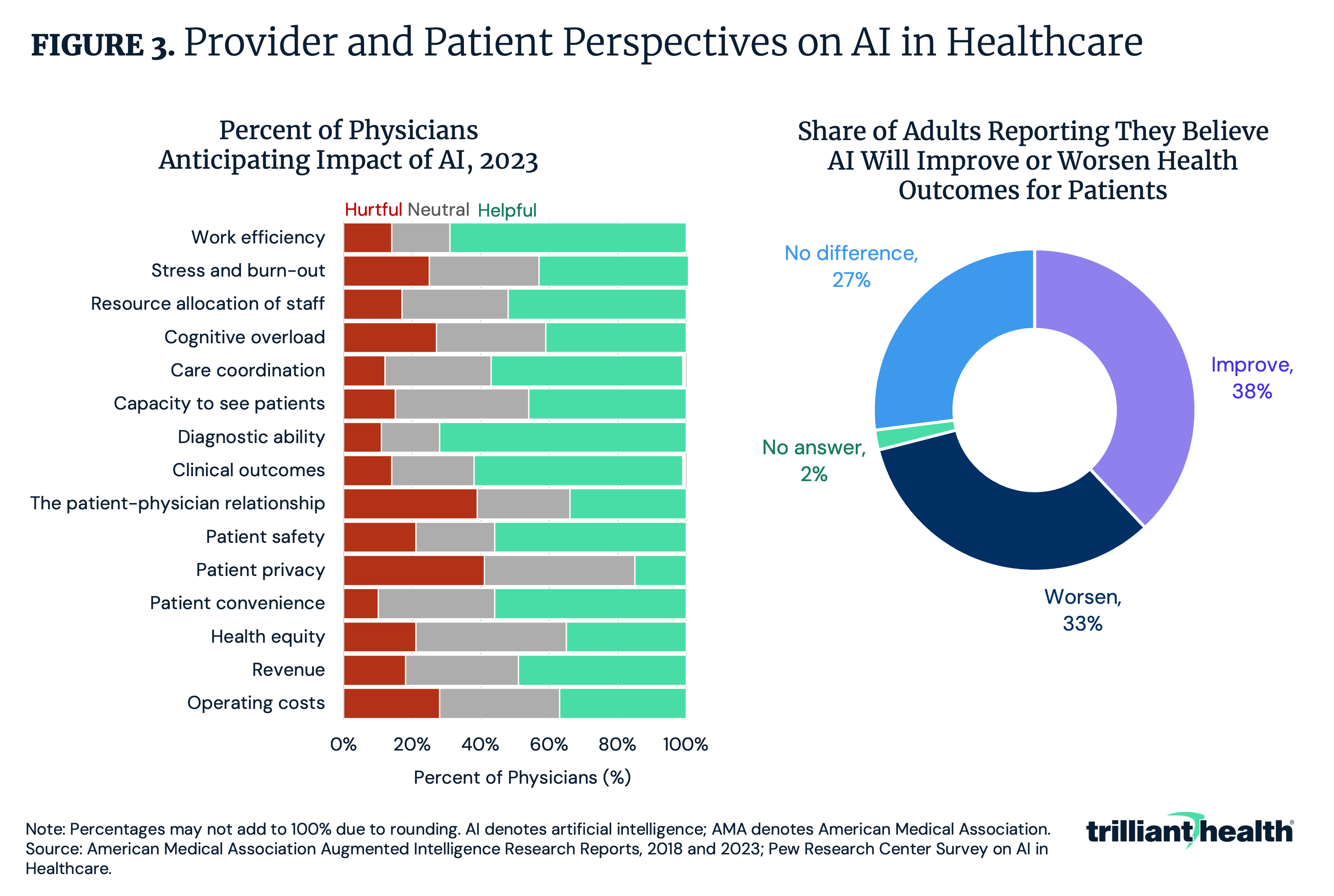

- Investment in AI care delivery technology is misaligned with patient and provider preferences. One third (33%) of patients report they believe AI will worsen outcomes for patients and another 27% believe it will have no impact, while 39% of providers are concerned that AI could damage the patient-physician relationship.

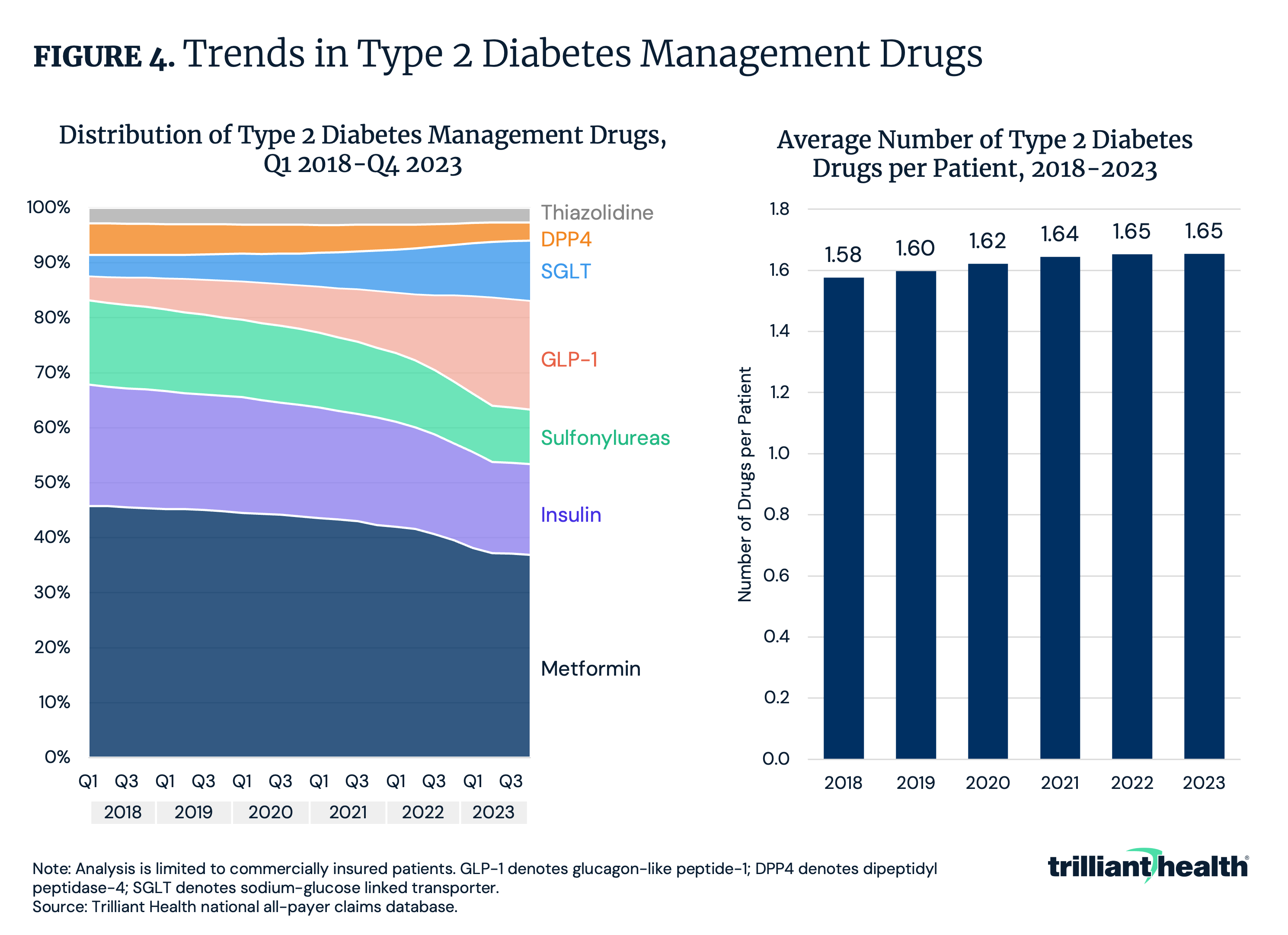

- Amid growth in the utilization of GLP-1s to treat type 2 diabetes, the average number of type 2 diabetes drugs per patient has increased from 1.58 in 2018 to 1.65 in 2023. At the same time, bariatric surgery volumes declined by 32.6%, reflecting the downstream impacts new therapies can have.

As discussed in our previous examinations of the Trends Shaping the Health Economy Report, the U.S. healthcare system is the most expensive in the world, with expenditures totaling $4.5T in 2022. This higher spending is attributable to several factors, including the declining health status of Americans, ineffective government regulation and higher price across healthcare services, including prescription drugs.1,2 Specifically, in 2022 the U.S. paid 422% more for branded prescription drugs than other OECD countries (Figure 1). Additionally, growth in spending on prescription drugs outpaces both growth in spending on hospital care and the consumer price index for all goods and services.

Clinical, technological and pharmaceutical innovations are critical to sustain and advance the revenue and profitability of those health economy stakeholders. However, the declining health status of Americans despite massive investments in innovation calls into question which, if any, advancements are creating value for the ultimate payers (i.e., Federal and state government and employers).

The Value of New Clinical Interventions Remains Uncertain

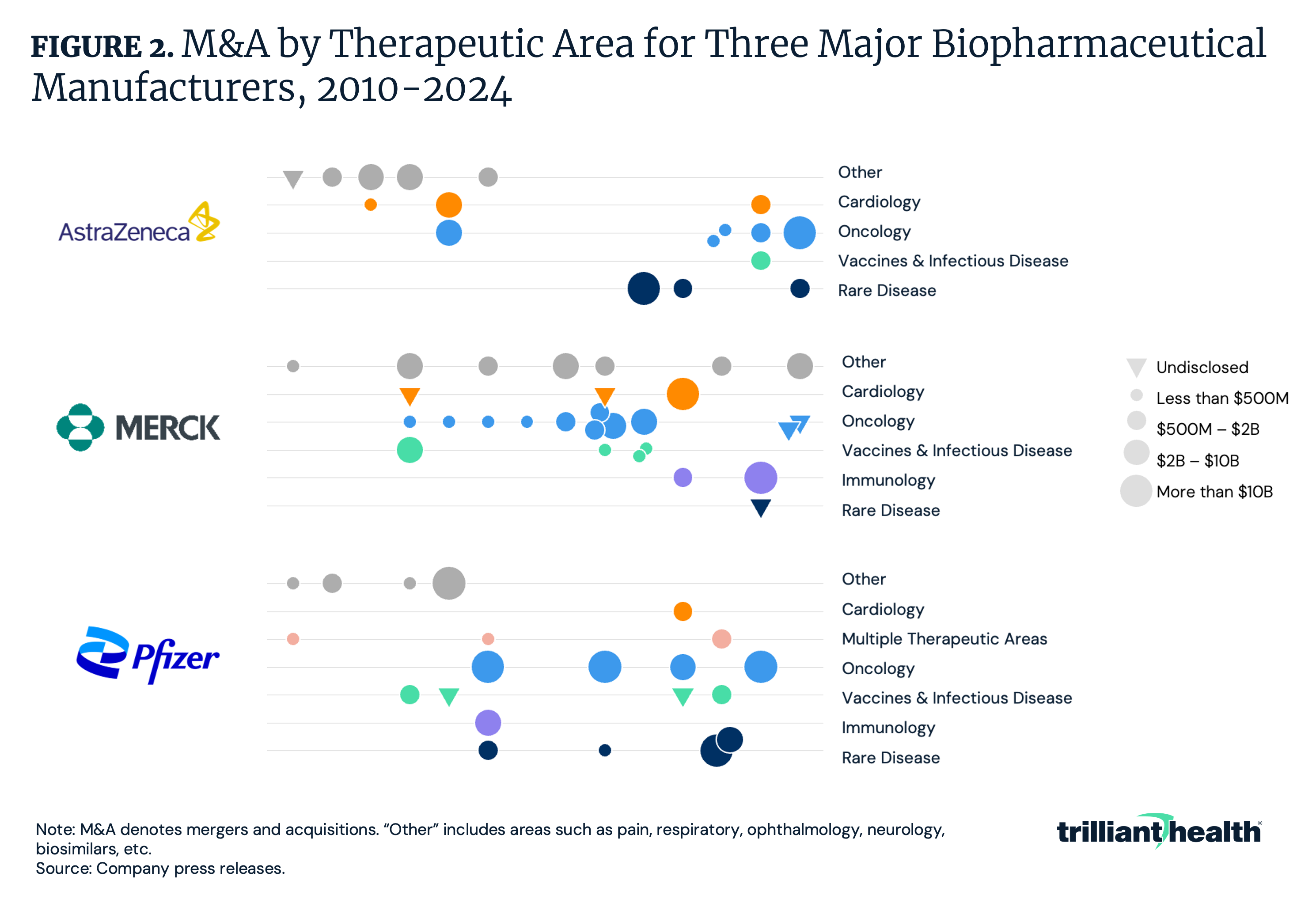

It is unclear whether new clinical advancements are leading to a net increase or decrease in value. In recent years, rare disease and oncology have garnered substantial focus and investment from large biopharmaceutical manufacturers. Notably, rare disease and oncology therapies are characteristically more expensive therapies than other therapeutic areas. Because rare disease treatments are often intended to be curative, often through a one-time administration of the drug, those treatments command a high price. For example, Lenmeldy™, a one-time treatment for metachromatic leukodystrophy, costs $4.25M per dose, making it the most expensive drug in the world.3

The potential to develop or acquire a “blockbuster” drug requires significant investment. Since 2020, AstraZeneca has invested $40.6B in rare disease through M&A and another $2.8B on oncology transactions (Figure 2). In contrast, Pfizer has invested $49.7B to acquire oncology-focused companies and $17B on rare disease-focused companies.

Whether the significant investments by life sciences companies will deliver a return on investment remains to be seen. There is a small patient cohort for many of the most expensive therapies, leading to questions about which entity – the Centers for Medicare and Medicaid Services (CMS), health insurers, employers – will pay for these treatments, which in turn requires a cost-benefit analysis that is ultimately a value judgment that impacts a specific patient.

For instance, metachromatic leukodystrophy effects only 1 in 40K people.4 While having a wide range of treatment options is important, it is equally critical to assess the cost-effectiveness of these therapies, particularly in a healthcare system that is not built on curative or preventive care. The impact of a treatment that is clinically proven to be curative is severely diminished if patients cannot afford it or if the system is not prepared to provide equal access.

Unlike countries with organizations that evaluate both the clinical and cost effectiveness of new prescription drugs during the approval process, such as the U.K.’s National Institute for Health and Care Excellence (NICE), U.S. regulators do not evaluate cost-effectiveness and accessibility. Notably, over 80% of the drugs approved in the U.S. since 2020 are not recommended by NICE, suggesting that many drugs are not providing value commensurate to their cost, even though the U.S. pays 2.7X more for these drugs than the U.K. pays.5 Ultimately, the benefits of an innovation cannot be fully realized if it is disconnected from affordability and access.

Despite Interest in Clinical Applications for AI, Utilization Trends and Patient and Provider Preferences Suggest AI is More Valuable in Other Areas

Similar to the friction between the development of high-cost therapies and mutually agreeable reimbursement for those therapies, there is often an incongruity between the engineering sophistication of a healthcare technology and its utility for patients and providers. Since 2018, CMS and other payers have agreed to reimburse multiple CPT codes that compensate providers for utilizing AI technologies in clinical settings. However, the aggregate associated patient volume for those codes totals only 201.7K over five years, with use concentrated among cardiac conditions.6

Limited utilization may be attributable in part to patient and provider attitudes regarding use of AI in care delivery. While most physicians report that AI will improve diagnostic ability (72%) and work efficiency (69%), 39% are concerned that AI could damage the patient-physician relationship and 41% report it could jeopardize patient privacy (Figure 3). Surveys have revealed that patients are less optimistic, with the majority reporting AI will either not impact (27%) or worsen (33%) health outcomes. To what extent can advancements in AI deliver value if both patients and providers have concerns about its safety? Should stakeholders continue to invest substantially in AI care delivery without understanding its realistic current and near-term applications? Conversely, will continued investment help to improve the trustworthiness and safety of AI in care delivery?

Expanded Drug Regimens Can Impact Spending Downstream

The value attributed to new therapies and technology are measured by the associated incremental costs as compared to cost savings from the reduction in other clinical treatments. For novel therapies, this cost will include potential increases in both side effects that increase utilization and the number of drugs needed to manage the specific clinical condition. For example, from 2018 to 2023 GLP-1s rose from the eighth most common type 2 diabetes drug regimen to the second most common.7 Simultaneously, the average number of type 2 diabetes drugs per patient increased from 1.58 in 2018 to 1.65 in 2023 (Figure 4). An increase in the average number of drugs used to manage a condition would deliver value for money if it leads to better patient outcomes, reduces the need for further treatments and ultimately lowers overall costs. However, despite expanded treatment options, the prevalence of type 2 diabetes increased between 2018 and 2022.8 With the proliferation of GLP-1s, it is critical to consider the long-term impact on American health relative to the amount invested in developing and paying for these medications. Ultimately, only extended monitoring of spending and health outcomes over time will reveal the value of emerging therapies like GLP-1s.

Emergence of New Therapies Impact Demand for Existing Treatments

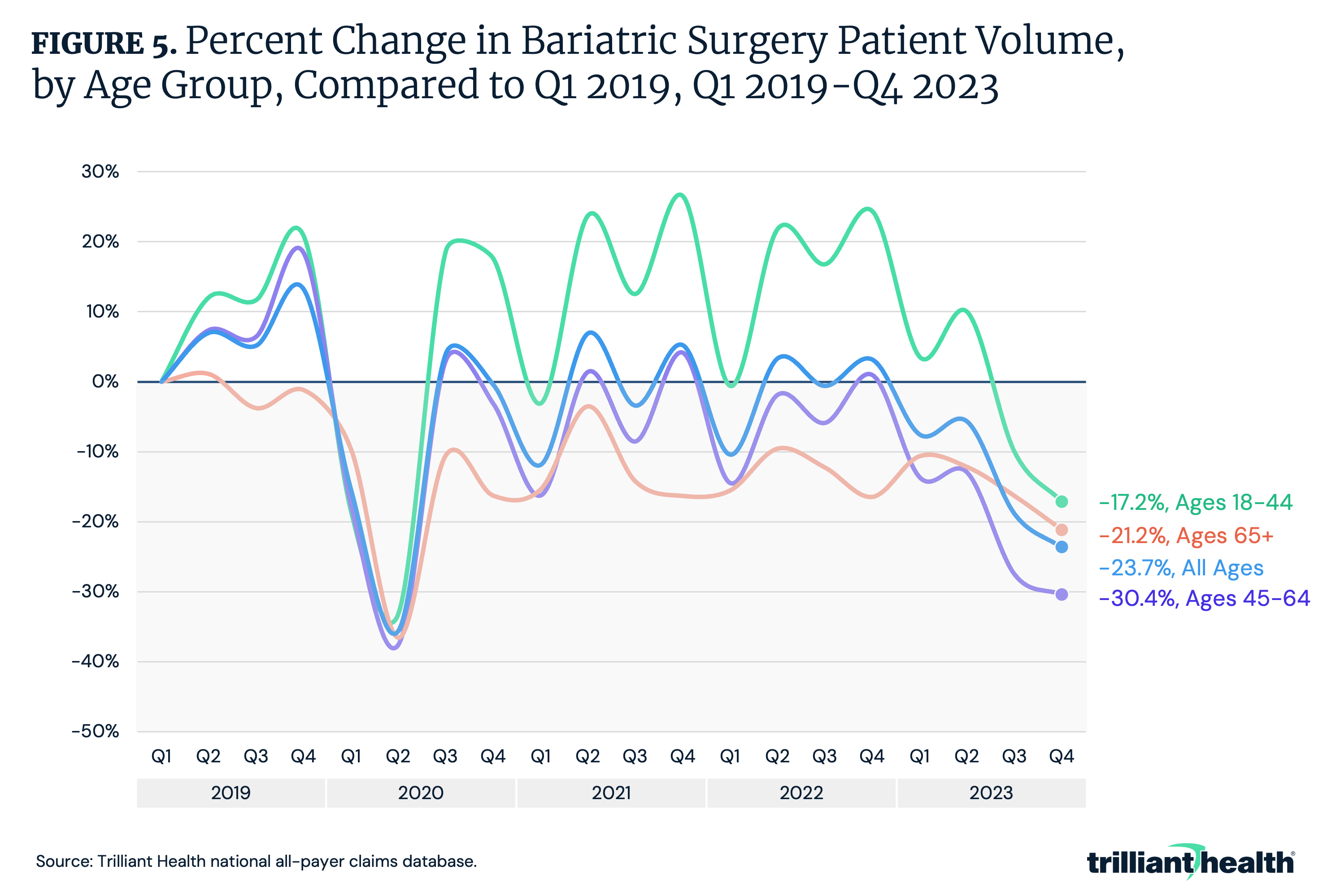

New therapies, like GLP-1s, can impact downstream demand for services. For instance, bariatric surgery was previously a common treatment for morbid obesity, although it is more invasive and costly when compared to GLP-1s. Evidence continues to emerge suggesting GLP-1s are effective tools for weight loss, and thus, tracking the impact of weight loss drugs on bariatric surgery over time is crucial. Bariatric surgery patient volume was 32.6% lower in Q4 2023 compared to Q4 2019 (Figure 5). While the declines in volume were more pronounced among patients ages 45 to 64 (-41.3%), utilization declined by 20.2% among patients ages 65 and older.

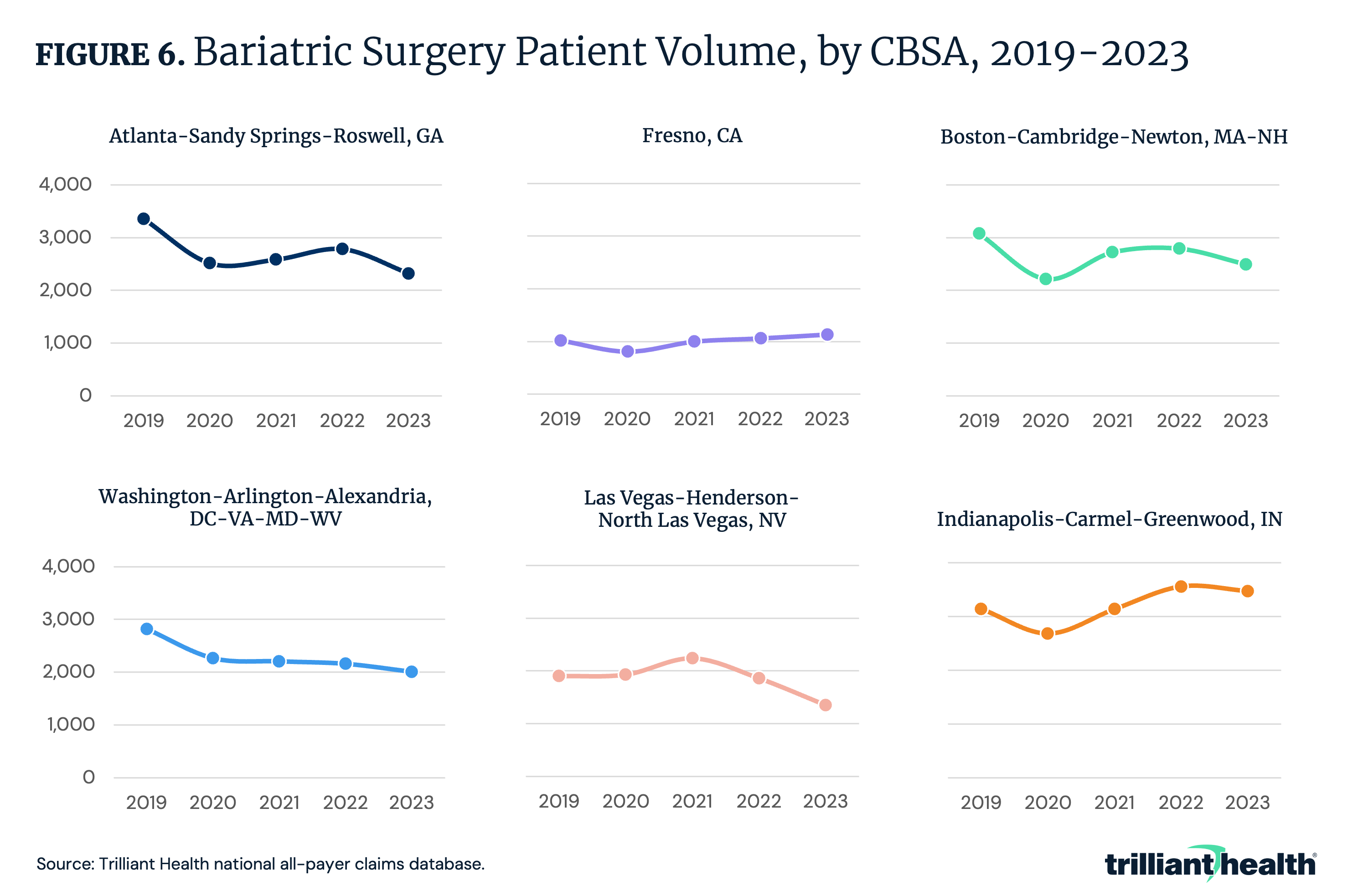

The change in bariatric surgery volume over time varies not just across age groups, but also across CBSAs. For instance, between 2019 and 2023, bariatric surgery volume declined in Atlanta-Sandy Springs-Roswell GA (-30.9%), Boston-Cambridge-Newton MA-NH (-18.9%), Las Vegas-Henderson-North Las Vegas NV (-28.9%) and Washington-Arlington-Alexandria DC-VA-MD-WV (-28.8%), while it increased by 11.1% and 10.7% in Fresno CA and Indianapolis-Carmel-Greenwood IN, respectively (Figure 6).

Conclusion

Technological advancements offer immense potential to revolutionize care delivery. However, their true value is only realized when innovations align with the needs and expectations of patients and providers, are accessible and offer benefits proportional to costs. Creating innovation without considering its broader implications tends to lead to value maximization for the innovator rather than value optimization for the health economy. Curative technologies and treatments may have limited impact if their pricing restricts access for those in need.

The declining health status of Americans presents an opportunity for innovations that address current and emerging patient needs. To seize this opportunity, healthcare stakeholders must adopt a long-term view that considers the total cost of care, patient preferences and the quality of less expensive, but effective, alternatives.