The Compass

Sanjula Jain, Ph.D. | November 5, 2023Key Takeaways

-

The growth of retail-based care has altered “traditional” care pathways, as an increasing number of consumer-friendly access points serve to fragment care coordination. Ultimately, these new care models and players are disintermediating “legacy” healthcare providers, making care more compartmentalized, transactional and detached.

-

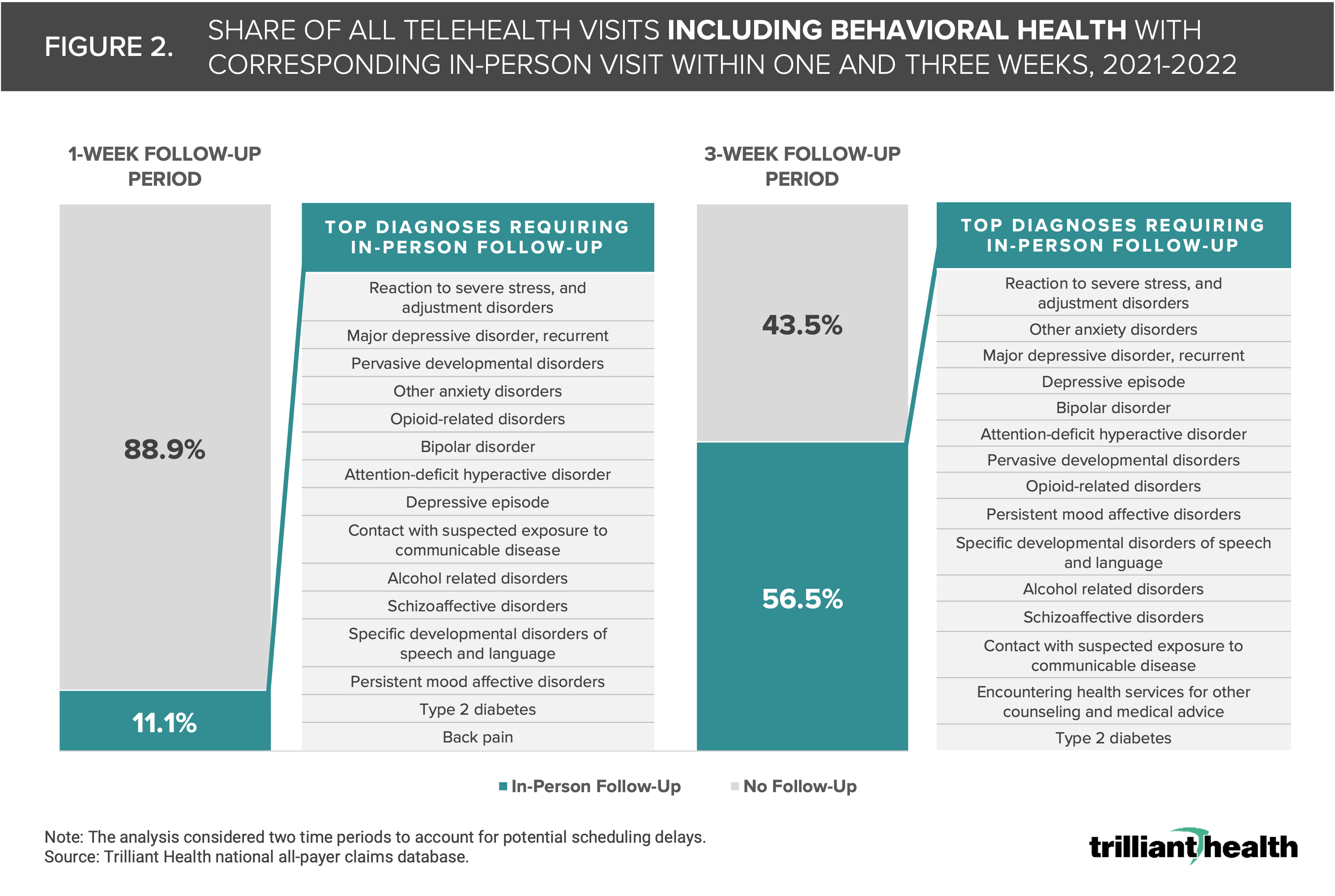

Between 2021 and 2022, 11.1% of telehealth visits for all conditions nationwide resulted in an in-person follow-up visit within a week for the same clinical reason. When expanding that timeframe to three weeks, the share of in-person follow-up visits increased to 56.5%, with behavioral health concerns making up most of the follow-up care.

-

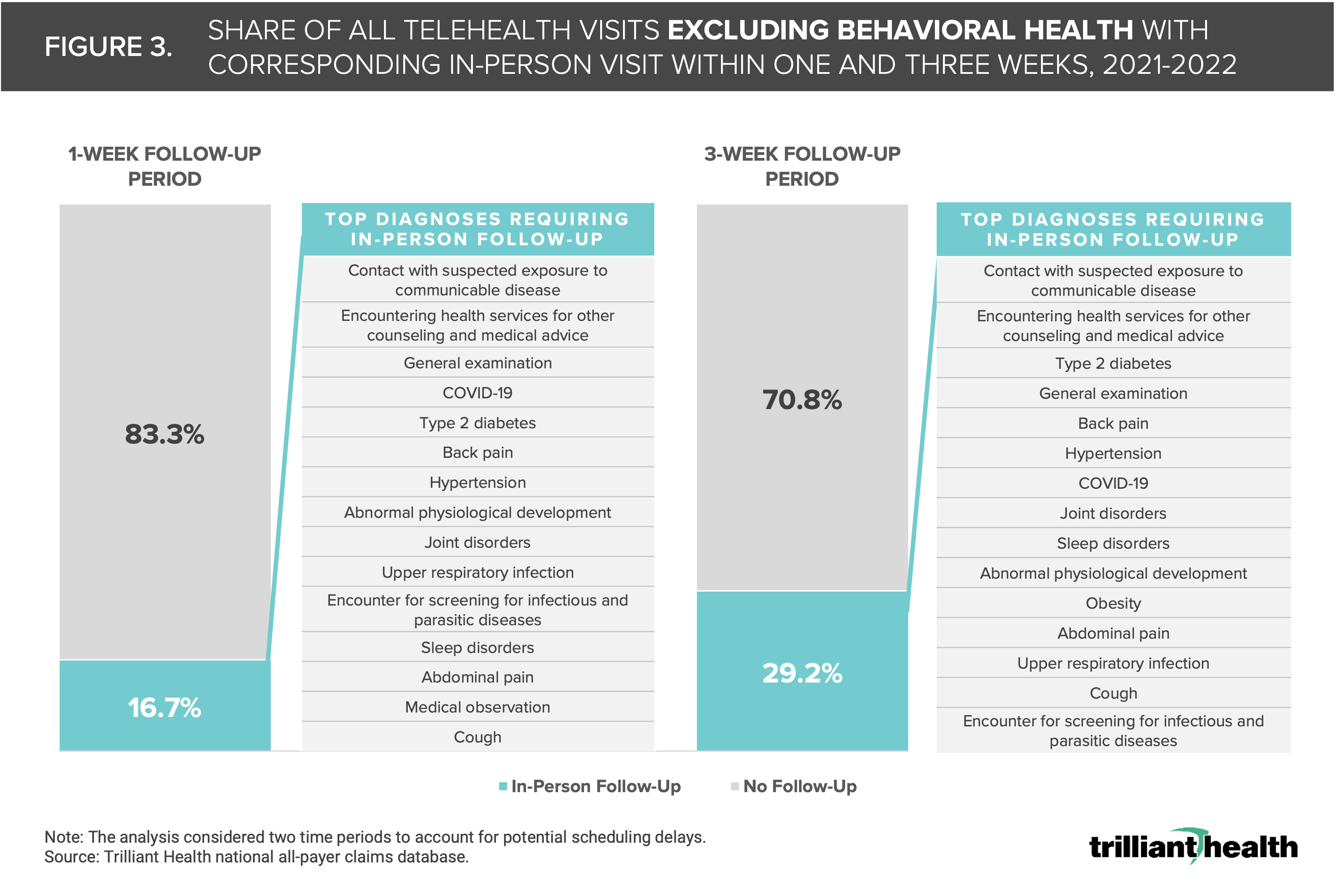

When behavioral health care was excluded, 16.7% and 29.2% of telehealth visits resulted in an in-person follow-up visit for the same clinical reason within one week and three weeks, respectively.

As we have previously discussed, patients increasingly make healthcare decisions like consumers, revealing a preference for on-demand care, with new primary care service offerings from large retailers like Amazon, CVS, Walgreens and Walmart as a catalyst. With their immense scale and strong consumer loyalty, these retailers are well positioned to cater to evolving patient preferences.1 Nevertheless, the growth of retail-based care has altered “traditional” care pathways, as an increasing number of consumer-friendly access points serve to fragment care coordination. Ultimately, these new care models and players are disintermediating “legacy” healthcare providers, making care more compartmentalized, transactional and detached.

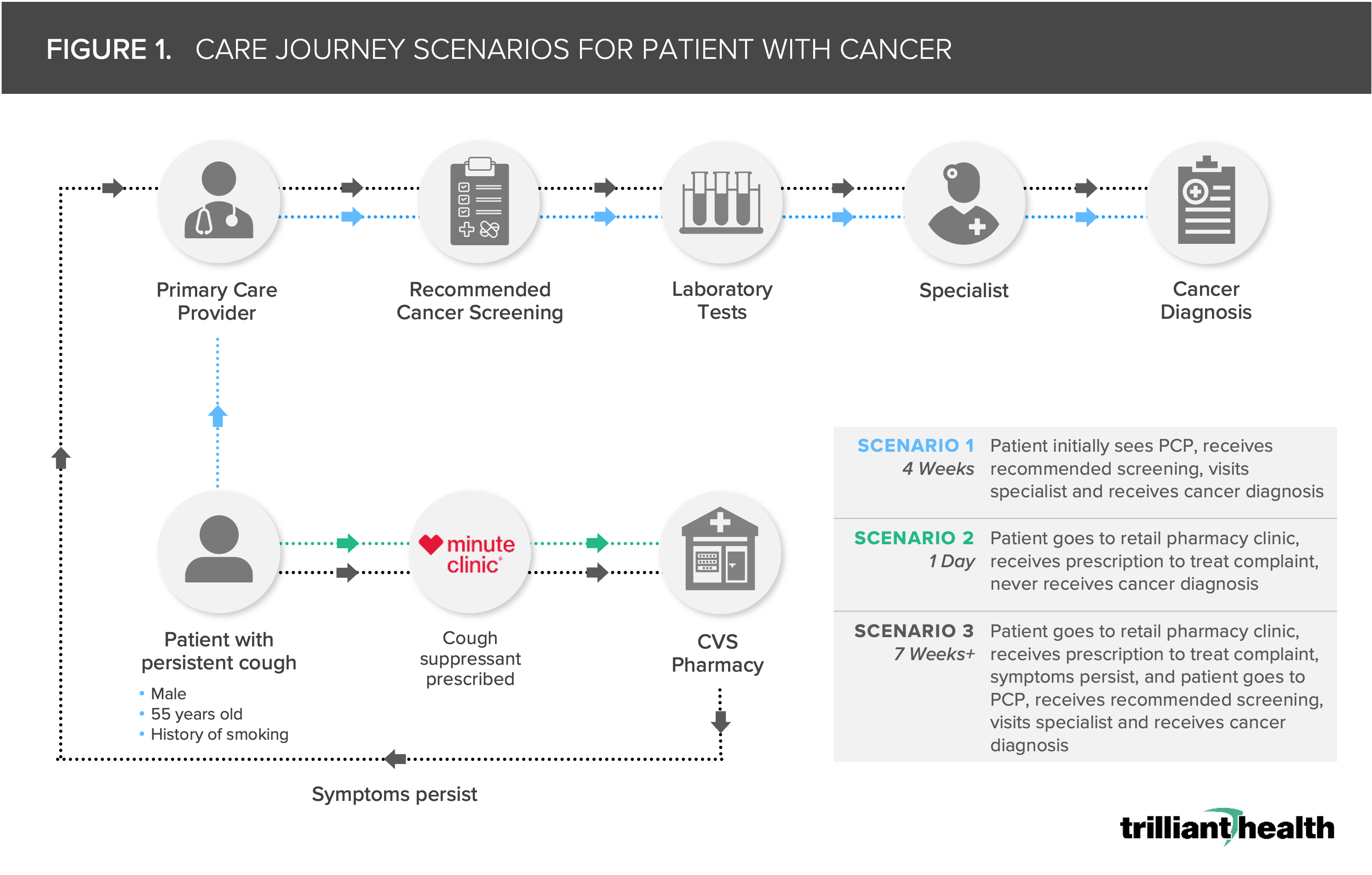

Different Care Journeys Reveal Disintermediation in Healthcare

Although retail players can meet a healthcare consumer’s desire for convenient care for low-acuity conditions (e.g., sinusitis), the lack of relationship between the consumer and retail provider encumbers a patient’s ability to navigate the system for the broader set of medical services they should receive (e.g., preventive screening). Traditional care models delivered by legacy providers are designed to be longitudinal, like an established primary care relationship to provide high-touch care or management of chronic conditions. In contrast, retail-based care models are functionally transactional, designed to disintermediate care by delivering discrete, well-defined services that target specific low-acuity conditions and bring patients into a closed-loop, retail-pharmacy-enabled system. The combination of downstream pharmaceutical revenue and operational scale allows large retailers to treat primary care delivery as a loss leader.2

To understand the implications of a patient’s care journey outside the “closed loop” system of retail or DTC models, consider three potential scenarios for a patient presenting with low-acuity symptoms but harboring a high-acuity condition (Figure 1). In the first scenario, a 55-year-old male with a history of smoking experiences a persistent cough. He promptly consults his primary care provider (PCP), who addresses the persistent cough but also conducts recommended screenings based on the patient’s medical history and arranges specialist consultations based on the screening result, leading to a swift cancer diagnosis and initiation of treatment within four weeks. In the second scenario, the same patient relies exclusively on a retail provider for the condition, receiving cough medicine but missing crucial screenings and, consequently, the cancer diagnosis. Even in the third scenario, where the patient eventually turns to his PCP and receives the cancer diagnosis after retail care couldn’t address his needs, his time to treatment is delayed as compared to what he would have received if he had initially sought care from his PCP.

For minor complaints like a cough, seeking care from a retail or DTC provider may save time and money. However, as these scenarios reveal, the transactional retail model is not designed for preventive or higher-acuity care. When patients require care beyond the retailer’s “closed loop” system, they face “friction costs” in terms of time, expenses, and potential health outcomes.

Is Telehealth Increasing Access or Creating Duplication of Service?

While the scenarios explored above are theoretical, analyzing actual patient journeys originating with a telehealth visit reveals the extent to which these providers often increase friction and duplicate care. For our analysis, we examined the frequency of telehealth visits resulting in in-person follow-up visits. Between 2021 and 2022, 11.1% of all telehealth visits nationwide resulted in an in-person follow-up visit within a week for the same clinical reason (Figure 2). When expanding that timeframe to three weeks, the share of in-person follow-up visits increased to 56.5%, with behavioral health concerns making up most of the follow-up care, reflecting the prevalence of omni-channel use.

When behavioral health care was excluded, 16.7% and 29.2% of telehealth visits resulted in an in-person follow-up visit for the same clinical reason within one week and three weeks, respectively (Figure 3). The predominant reasons for these follow-up visits were general encounters and chronic condition management.

When behavioral health care was excluded, 16.7% and 29.2% of telehealth visits resulted in an in-person follow-up visit for the same clinical reason within one week and three weeks, respectively (Figure 3). The predominant reasons for these follow-up visits were general encounters and chronic condition management.

It is striking that even for tele-behavioral health, which the data suggest is a viable substitute for in-person care, care duplication is frequent.3 While retail and DTC models are primarily utilized for low-acuity care, patients are increasingly seeking out chronic condition management (e.g., diabetes, major depression) from these models ill-suited for those needs. Retail and DTC providers offer segmented care and struggle to maintain a sustained patient-provider relationship or provide continuous monitoring and preventive care. Patients needing care beyond these closed loop systems inevitably encounter friction costs in the form of wasted time, duplicative costs and potentially adverse long-term health outcomes.

As we have previously discussed, the data reveal the younger adult, commercially insured population that prefers retail-based care is the same population that is also experiencing increasing morbidity and mortality (i.e., neoplasm deaths increasing in ages 35-44, more deaths attributed to overdose in individuals under age 40). What tradeoffs are Americans willing to make for convenience-based care, and do they understand these tradeoffs? If not, what role will payers, employers and providers play in educating consumers about these tradeoffs?

Primary care in the U.S. is already splintered, patient acuity is worsening and the pandemic has exacerbated these trends by leading to declines in routine screenings and essential services.4,5,6,7 The U.S. health economy is already grappling with poor care coordination among established providers, and the introduction of additional pathways by DTC and retail providers has further fragmented patient navigation of the complex healthcare ecosystem. While consumer-centric care models have obvious benefits, there are significant implications for how consumers adopt, and other stakeholders adapt to, these transactional care models. Next week, we will continue to explore the effects of retail and new entrant delivery models on the health economy, but from the supply side.

Log in to the Compass+ platform to access additional insights on the topic of healthcare commoditization, disintermediation and specialty care.

Disintermediation and Commoditization of Healthcare is Not Restricted to Primary Care

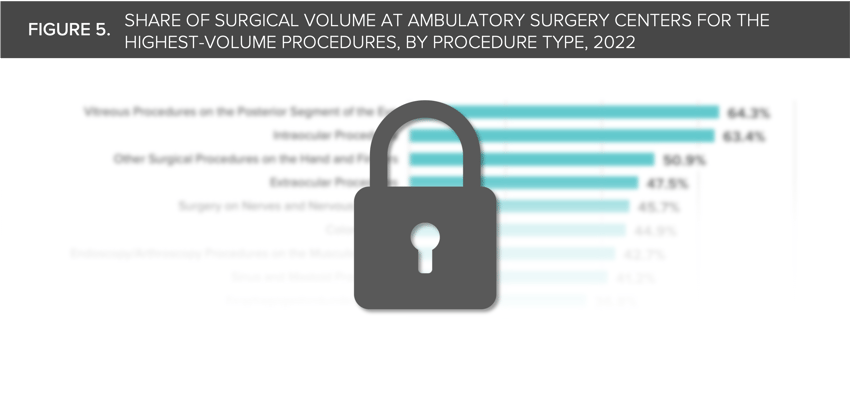

While we have focused extensively on new entrants and disintermediation of low-acuity care, higher-acuity conditions, including those needing surgery, are not exempt from the trend towards having more options for accessing care. For years, surgical care has steadily migrated to outpatient settings, particularly ambulatory surgery centers (ASCs), whose share of volume increased from 21.8% to 22.2% between 2021 and 2022. From 2017 to 2022, the surgical procedures with the highest volume growth at ASCs were total knee or hip replacements (335.3%) and arterial and veinous procedures (+184.9%), while arterial and veinous ligation procedures (-36.5%) and proctoscopies (-29.8%) decreased most (Figure 4).

- New Entrants

- Specialty Care

- Virtual Care

- Behavioral Health

- Healthcare Consumerism

See more with Compass+

You are currently viewing the free version of this study. To access the full study, subscribe to Compass+ Professional for $199 per year.

Sign Up for Compass+Interested in citing our research? Please follow this guide.