The Compass

Sanjula Jain, Ph.D. | June 23, 2024Key Takeaways

- Health systems are increasingly investing in digital front doors and virtual strategies with the hope of enhancing patient engagement, continuity of care and downstream capture, the effectiveness of which should be measured by share of care, which quantifies the financial impact of patient loyalty and retention.

- In comparing in-system downstream care from 2021 to 2022, one health system did not see meaningful change, while capture rates increased for others. Roughly 20% to 35% of inpatient care and 60% to 75% of outpatient care was rendered outside of the systems analyzed, highlighting an opportunity to capture more high-acuity follow-up care prompted by “front door” interactions.

- Compass+ Exclusive for Digital Health Leaders: Quantifying Telehealth Patient Volumes and Health System Patient Affiliation

You are currently viewing the public version of The Compass.

To unlock additional analyses, upgrade your subscription to the Compass+ Portal.

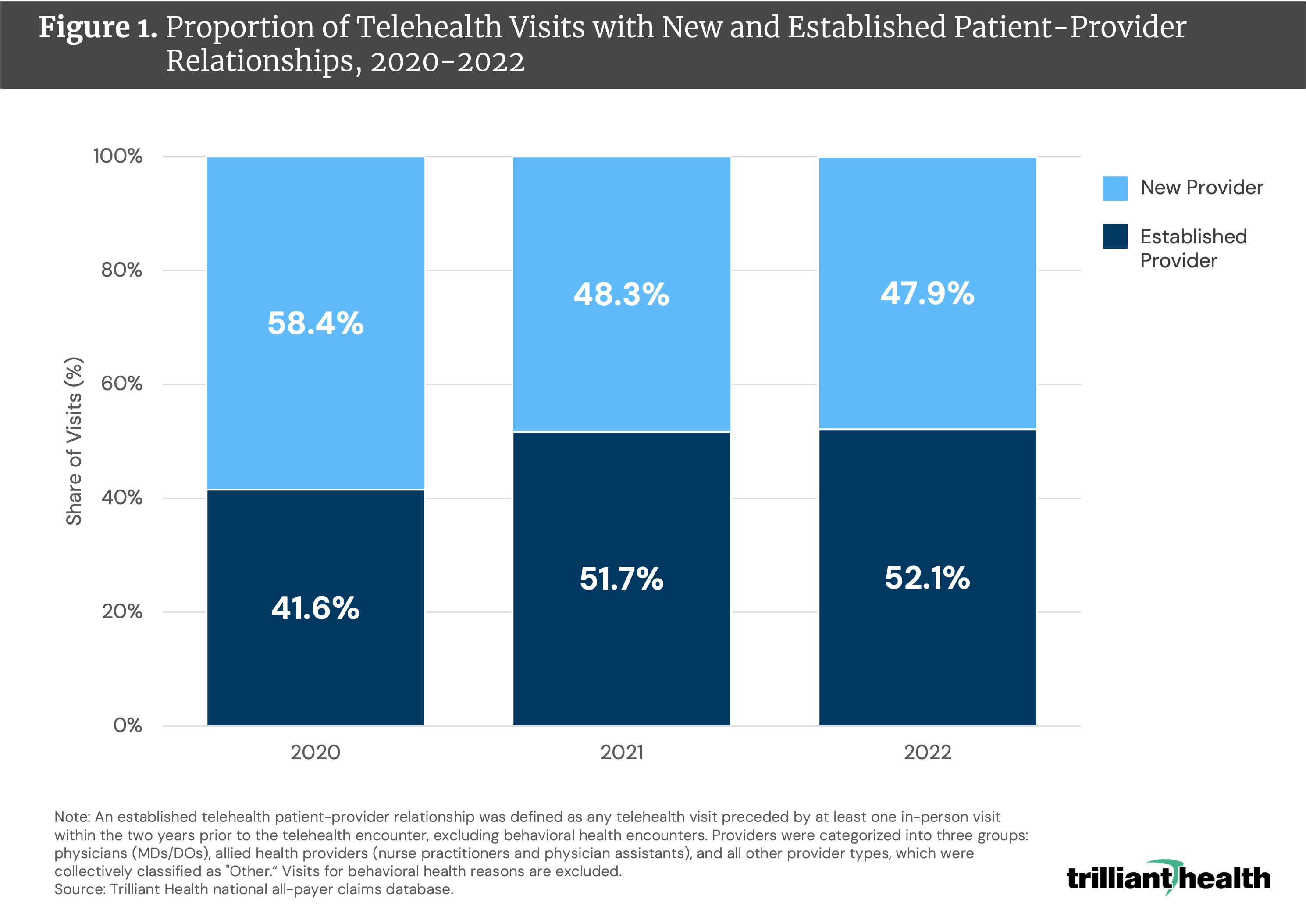

In the previous two editions of The Compass, we analyzed key telehealth utilization and provider supply trends.1,2 We found that 1) aggregate demand is declining and concentrating around behavioral health, further justifying the market exit decisions of Walmart and UnitedHealthcare, and 2) only half of telehealth visits are rendered by established providers, posing the risk of fragmentation of traditional primary care models.

In synthesizing the data about demand for and clinical utility of telehealth in the context of minimal technological barriers to market entry, health systems should reassess their digital health strategies, many of which were rapidly implemented in response to the pandemic. Such an assessment should evaluate the effectiveness of telehealth and other access points in maintaining continuity and quality of care, fostering consumer loyalty and generating high-yield downstream care. If telehealth’s use is limited to a discrete set of clinical services, how effectively can it serve as a "digital front door" for health systems whose financial results depend on high-margin surgical services?

Background

Prior to the COVID-19 pandemic, health systems began to invest broadly in digital front doors – virtual platforms that patients use to access healthcare services, resources, appointment scheduling, medical records and provider messaging. In theory, the digital front door offers consumer-friendly, low-acuity engagement to improve patient loyalty, resulting in a greater capture of downstream services. The primary services offered by the digital front door are typically low margin "loss leaders," which health system executives acknowledge are not highly profitable but believe can serve as a precursor to more lucrative acute care services.

The high expectations associated with digital front doors are reflected in a recent McKinsey survey of health system executives. About 70% of respondents reported high investment priority and anticipated organizational impact for digital front doors and, more broadly, virtual health integration.3

Having expanded digital strategies rapidly in response to the COVID-19 pandemic, health systems should reconsider the long-term benefits of the digital strategies that emanated from the “forced adoption” prevalent in the pandemic. Since 2020, it has become increasingly evident that telehealth poses the potential to disrupt care continuity for patients. In revisiting digital strategies, health systems should employ a service-line-specific approach to identify the most clinically appropriate usage of virtual care in the context of other access points and delivery mechanisms for care. Share of care, which quantifies the financial impact of patient loyalty and retention, is the most reliable measure of the success of any access point to a health system, whether a digital front door or the entrance to the emergency department.

Analytic Approach

Leveraging our national all-payer claims database and Provider Directory, we examined care utilization within and outside of three geographically diverse U.S. health systems with 2023 revenue exceeding $10B for patients that received telehealth care within each system. “Health System A” serves Southwest markets, “Health System B” serves Midwest markets and “Health System C” serves Southeast markets. We analyzed inpatient, outpatient, emergency and telehealth utilization in 2021 and 2022 following an associated telehealth encounter with the health systems included in the analysis.

Findings

Among the patients that utilized telehealth services within these health systems, we analyzed the downstream share of care retained within the same system to measure the effectiveness of the digital front door. In comparing in-system downstream care from 2021 to 2022, Health System A did not see meaningful increases, while capture rates increased for Health Systems B and C. Because there are fewer options for inpatient than outpatient care in every market, inpatient care represented the highest downstream capture rates: Health System A (64.8%, 64.1%), Health System B (62.8%, 69.8%) and Health System C (70.3%, 78.3%) in 2021 and 2022, respectively (Figure 1). Conversely, outpatient capture rates were significantly lower among the health systems analyzed: Health System A (23.9%, 25.5%), Health System B (35.3%, 38.6%) and Health System C (23.1%, 24.8%) in 2021 and 2022, respectively. Roughly 20% to 35% of inpatient care and 60% to 75% of outpatient care was rendered outside of those systems, reflecting an opportunity to capture more high-acuity follow-up care prompted by “front door” interactions. Downstream capture rates for telehealth and emergency care ranged from 39.0% to 68.7% and 48.6% to 67.7%, respectively.

Compass+ Exclusive for Digital Health Leaders: Quantifying Telehealth Patient Volumes and Health System Patient Affiliation

Unlock the complete analysis with Compass+

Conclusion

The most important conclusions from our three-part series are as follows:

- Telehealth utilization trends indicate that consumers largely view telehealth as an appropriate substitute for low-acuity in-person behavioral health treatment but less frequently for chronic condition management or cancer treatment. While there are viable business models leveraging virtual care, the current market is unsustainable, and pandemic-era market expectations will never materialize.

- Telehealth presents a paradox: the potential to enhance access and convenience for discrete clinical scenarios coupled with the risk of fragmentation when patients frequently interact with providers lacking established patient relationships or access to their medical history. With the skepticism around its broad applicability and effectiveness from providers and employers, together with hesitancy from Federal policymakers to permanently codify pandemic-era Medicare telehealth flexibilities, the virtual care industry is not likely to expand at the pace or magnitude that digital health companies want.

Having made substantial investments in virtual care strategies based on enthusiasm for potential benefits, health systems must now monitor and measure the impact that digital front doors and virtual care have on downstream capture and patient acquisition, satisfaction and alignment. Because the financial success of these strategies depends upon clinical condition, patient preferences and market dynamics, continuous monitoring of these metrics is essential to distinguish the performance of “digital front door” strategies from their potential.

Whether telehealth can improve care coordination is another consideration that requires understanding the longitudinal patient journey of individuals using telehealth, both within and outside of health systems. What patients are using telehealth for, who renders the virtual care, where patients go next and how the virtual encounter influenced their overall care journey defines which types of digital front door interactions can be useful.

Given the variable capture rates across care settings and the limited clinical utility of telehealth, the data suggest the digital front door may not be as effective as health system executives anticipate. Moreover, as more nontraditional competitors enter the healthcare delivery market, health systems will be challenged to increase consumer loyalty for low-acuity and increasingly commoditized care. Whether telehealth as the digital front door can generate a return on invested capital is a question for every health system, the answer to which requires measuring where telehealth patients are pursuing care – both within and outside the health system – to quantify loyalty and patient alignment.

Thanks to Colin Macon and Katie Patton for their research support.

- Virtual Care

- Healthcare Consumerism

- Healthcare Investments & Partnerships

- Patient & Provider Loyalty

See more with Compass+

You are currently viewing the free version of this study. To access the full study, subscribe to Compass+ Professional for $199 per year.

Sign Up for Compass+Interested in citing our research? Please follow this guide.