.png)

.png?width=171&height=239&name=2025%20Trends%20Report%20Nav%20(1).png)

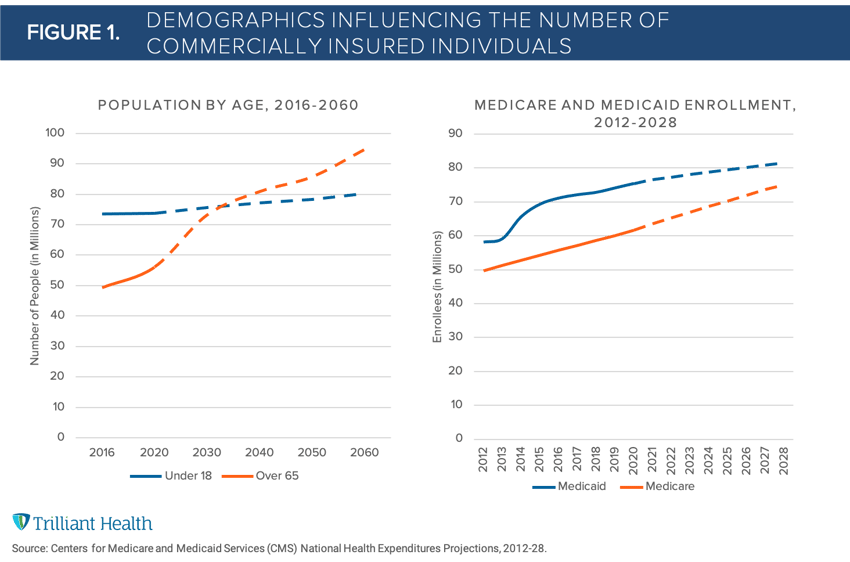

Last week, CMS released its latest Medicaid enrollment numbers reporting a record number of enrollees during the pandemic. An additional 9.7M individuals enrolled in Medicaid from February 2020 to January 2021 totaling approximately 73.8M Medicaid beneficiaries at the beginning of 2021. The projected growth in the nation’s safety net program compounded by more Baby Boomers aging into Medicare will significantly reduce the share of patients covered by commercial insurance (Figure 1).

The declining number of commercially insured individuals, however, was a trend even prior to COVID-19. On average, 50% of total revenues of the largest health systems were attributed to government payments pre-pandemic. To offset the lower reimbursements attributed to caring for Medicare and Medicaid patients, health systems have historically relied on revenue from their commercially insured patients to subsidize.

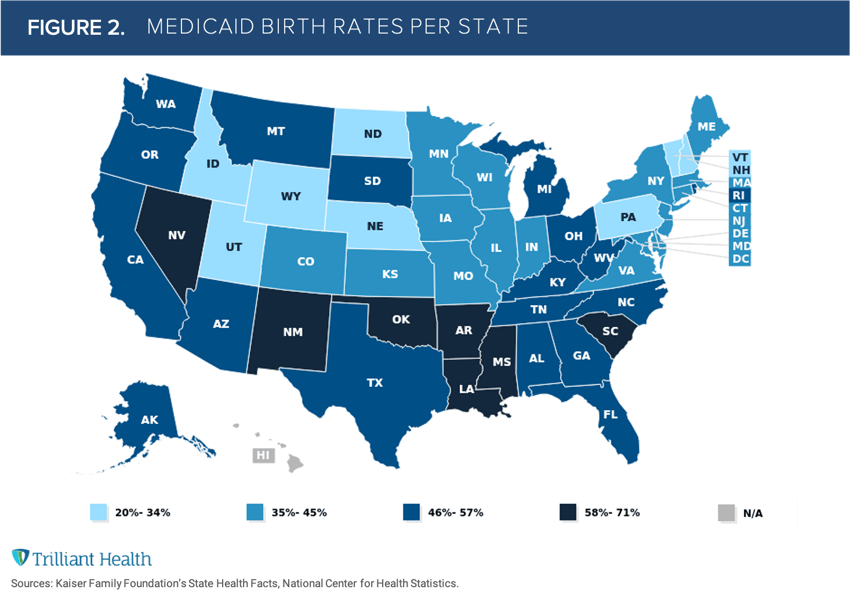

The number of projected births is insufficient to outpace the increase in Medicare enrollment from the Baby Boomers. Moreover, nearly 50% of new births are financed by Medicaid with the fastest growing states (the Sunbelt region) representing above average Medicaid birth rates (Figure 2). Thus, the post-pandemic health economy will be defined by an even smaller commercially insured population, forcing health systems to re-evaluate their longstanding growth strategies.

As more suppliers enter the care delivery market, a greater number of providers will be competing for an even smaller share of “target” patients. Brands like Walmart will make the competition for health systems even more difficult, not only in terms of scale of “consumer stickiness” but on price.

Whereas traditional providers have operated in a health economy with prices and reimbursements varying by market and payer type, new players like Walmart are opting for a simpler, low-cost model. As previously shown, Medicaid is no longer setting the floor for primary care visits. Inevitably, these market dynamics will create even greater downward pressure on commercial rates.

As post-pandemic realities accelerate the growth in the number of publicly insured individuals, health systems that can effectively leverage psychographic and consumer loyalty data to both increase current share of care from existing commercial patients, and identify which individuals have the potential to split their share of commercial care across more brands will maintain a competitive advantage.